New Elements of SOC 2

In April 2017, the AICPA issued several updates to SOC 2 reporting. The most noticeable change is the revision from “Trust Services Principles and Criteria” to “Trust Services Criteria.” Other updates include points of focus, supplemental criteria, and the inclusion of the 17 principles from the 2013 COSO Internal Control Framework. Let’s take a look at how these principles will be used in a SOC 2 report.

Updates to the COSO Internal Control Framework

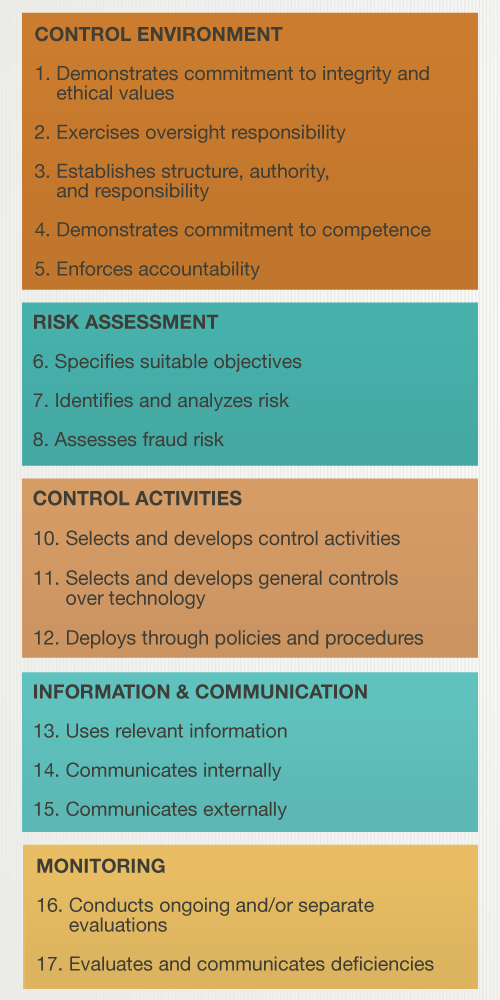

The COSO Internal Control Framework is used to assess the design, implementation, and maintenance of internal controls and assess their effectiveness. While the five basic components of the COSO Internal Control Framework – control environment, risk assessment, control activities, information and communication, and monitoring activities – have not changed, the 17 principles of principles of internal control that are aligned with each of the five basic components. Additionally, there are now 81 points of focus across these 17 principles.

What are the 17 Principles of Internal Control?

The introduction of these 17 principles of internal control allow for organizations to have an explicit understanding of what each of the five basic COSO components requires, making it easier for organizations to apply them. Every organization pursuing a SOC 2 report, regardless of size, must demonstrate that each of the 17 principles of internal control are present, functioning, and operating in an integrated manner. An organization’s ability to satisfy each of the five components and their subsequent principles demonstrates that they have an effective system of internal controls. The 17 principles of internal control include:

The 17 internal control principles do not map to the 2016 Trust Services Principles and Criteria, so this new integration with the 2013 COSO framework will likely require service organizations to restructure their internal controls in order to comply with the 2017 Trust Services Criteria.

More SOC 2 Resources

Understanding Your SOC 2 Report

SOC 2 Compliance Handbook: The 5 Trust Services Criteria

[av_toggle_container initial=’1′ mode=’accordion’ sort=” styling=” colors=” font_color=” background_color=” border_color=” custom_class=”]

[av_toggle title=’Video Transcript’ tags=”]

The AICPA issued new SOC 2 Trust Services Criteria in 2017. These criteria must be used for any reports issued after December 15, 2018. Until that date, you have the option of using the 2016 criteria or the 2017 criteria.

One of the big things that is new in the 2017 criteria is the inclusion of the 17 principles from the COSO Internal Control Framework. These 17 principles have to do with things dealing with governance of the organization, how you communicate issues to the employees within your organization, how you perform risk assessments, or how you monitor your controls.

You can reference some of our other materials on the COSO Internal Control Framework and also visit our web portal, where you can find resources on this topic.

[/av_toggle]

[/av_toggle_container]